Navigating the RV Insurance Maze: A Guide for RV Clarity Readers

Navigating the world of RV insurance can feel like driving a 40-foot Class A through a narrow mountain pass—intimidating, but manageable with the right map. For RV Clarity readers, understanding that your RV is both a vehicle and a home is the first step toward avoiding costly coverage gaps.

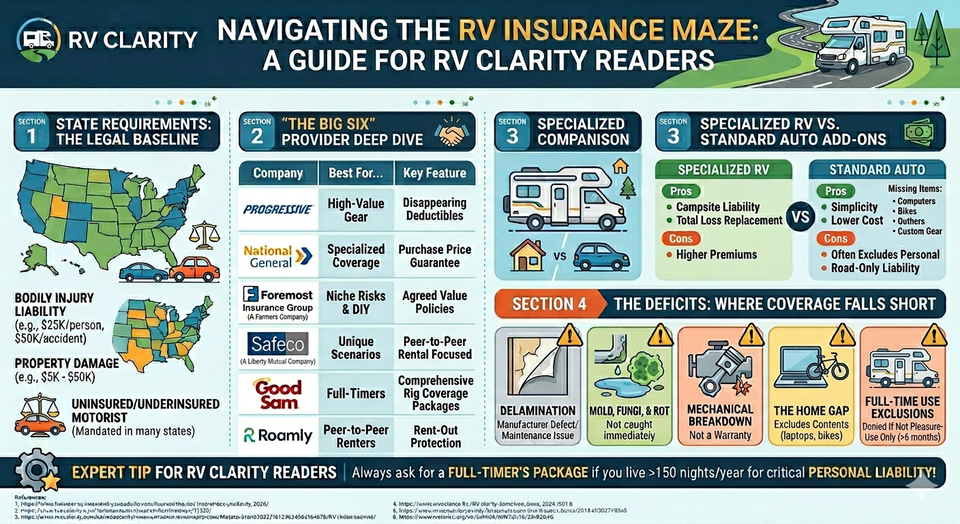

Here is a breakdown of the current landscape for RV insurance in 2026, including state requirements, the pros and cons of different policy types, and the hidden deficits you need to watch out for. 1. State Requirements: The Legal Baseline

Just like a standard car, self-propelled RVs (motorhomes) must meet state-specific liability minimums. However, towable RVs (travel trailers, 5th wheels) are usually covered for liability by the tow vehicle’s policy, though separate comprehensive and collision coverage is highly recommended. 2. Provider Deep Dive

Choosing the right provider often depends on whether you are a weekend warrior or a full-time nomad. Here is how the industry giants stack up:

National General (An Allstate Company) 3. Pros vs. Cons: Specialized RV vs. Standard Auto

Many owners make the mistake of simply adding their RV to an existing auto policy. While convenient, it often leaves you exposed.

Specialized RV Insurance 4. The Deficits: Where Coverage Falls Short

Even with a "full" policy, certain gaps can leave you paying out of pocket. 💡 Expert Tip for RV Clarity Readers

Always ask for a "Full-Timer's Package" if you spend more than 150 nights a year in your rig. Without it, companies may treat your RV as a "secondary vehicle," which lacks critical personal liability protection you need if someone trips and falls under your awning. References

Here is a breakdown of the current landscape for RV insurance in 2026, including state requirements, the pros and cons of different policy types, and the hidden deficits you need to watch out for.

Just like a standard car, self-propelled RVs (motorhomes) must meet state-specific liability minimums. However, towable RVs (travel trailers, 5th wheels) are usually covered for liability by the tow vehicle’s policy, though separate comprehensive and collision coverage is highly recommended.

- Bodily Injury Liability: Most states require a minimum of $25,000 per person and $50,000 per accident. States like Alaska and Maine demand higher limits ($50,000/$100,000), while California and Florida have lower thresholds.

- Property Damage: Requirements vary significantly, from as low as $5,000 in Massachusetts to $50,000 in North Carolina.

- Uninsured/Underinsured Motorist: Many states (e.g., Illinois, Oregon, Connecticut) mandate this to protect you if you're hit by someone without adequate insurance.

Choosing the right provider often depends on whether you are a weekend warrior or a full-time nomad. Here is how the industry giants stack up:

National General (An Allstate Company)

- Best For: Specialized Coverage.

- The Edge: Their Purchase Price Guarantee. If your rig is totaled within its first 9 years, they pay you what you originally paid for it, not its depreciated market value.

- The "Catch": They are aggressive with "Storage Savings." If you forget to reactivate road coverage before a quick weekend trip, you have zero protection the moment you leave the driveway.

- Best For: Overall Value.

- The Edge: Disappearing Deductibles. For every claim-free period, they knock 25% off your deductible until it hits $0.

- The "Catch": Strictness regarding "Gradual Damage." If a windstorm rips your roof, but an adjuster finds pre-existing sealant cracks, they may deny the claim due to "lack of maintenance."

- Best For: High-Value Gear.

- The Edge: Personal Effect Coverage. They offer higher limits for the "stuff" inside your RV (cameras, computers, outdoor gear) than standard insurers.

- The "Catch": Custom Equipment caps. Your $20k solar array might be capped at a default amount (e.g., $3,000) unless specifically scheduled on the policy.

- Best For: Niche Risks & DIY.

- The Edge: Specialized Valuations. They excel at "Agreed Value" policies for vintage Airstreams or custom van conversions.

- The "Catch": Strict Animal Exclusions. They may have tighter liability restrictions regarding specific dog breeds.

- Best For: Full-Timers.

- The Edge: Specializes in comprehensive packages specifically designed for those living in their rig.

- The "Catch": Often requires a membership fee to access certain rates or specialized benefits.

- Best For: Peer-to-Peer Renters.

- The Edge: Designed specifically for owners who plan to rent their RV out to others, filling a gap most traditional policies exclude.

- The "Catch": May lack some of the deep "total loss replacement" perks found in older, established carriers.

- Best For: Customer Service.

- The Edge: Consistently high satisfaction ratings and low complaint volume through a network of independent agents.

- The "Catch": Coverage is only available in certain states and requires working through an agent rather than a direct online portal.

Many owners make the mistake of simply adding their RV to an existing auto policy. While convenient, it often leaves you exposed.

Specialized RV Insurance

- Pros: Includes Campsite Liability (covers injuries that happen while parked), Total Loss Replacement, and coverage for specialized equipment like solar arrays or satellite dishes.

- Cons: Generally, more expensive than a basic auto add-on.

- Pros: Lower premiums and the simplicity of a single bill.

- Cons: Often lacks coverage for personal belongings (electronics, kitchenware) and may only cover the RV while it is in motion on the road.

Even with a "full" policy, certain gaps can leave you paying out of pocket.

- The "Home" Gap: Standard vehicle policies often ignore the contents of the RV. If your laptop or bike is stolen from the rig, a standard auto policy likely won't cover it.

- Full-Time Use Exclusions: If you live in your RV more than 6 months a year but only have a "pleasure use" policy, your claim could be denied entirely.

- Storage Deficits: Look for "Storage Option" policies that suspend collision coverage while parked to avoid overpaying during winter months.

- Maintenance Denials: Most companies do not cover delamination, mold/rot from slow leaks, mechanical breakdowns, pest damage, or damage from freezing due to improper winterization.

Always ask for a "Full-Timer's Package" if you spend more than 150 nights a year in your rig. Without it, companies may treat your RV as a "secondary vehicle," which lacks critical personal liability protection you need if someone trips and falls under your awning.

- Atrium Insurance Group. (2025). How RV insurance differs from auto insurance and why it matters.

- JD Power. (2026). How do states vary in coverage requirements for RV insurance?

- InsuredBetter.com. (2026). The best RV insurance companies of 2026.

- Money. (2026). 6 best RV insurance companies of May 2026.

- Quality Irving. (2025). The difference between RV and auto insurance: Why do you need specialized coverage.

- Scautub. (2025). What does RV insurance cover and how to avoid common mistakes?